")

")

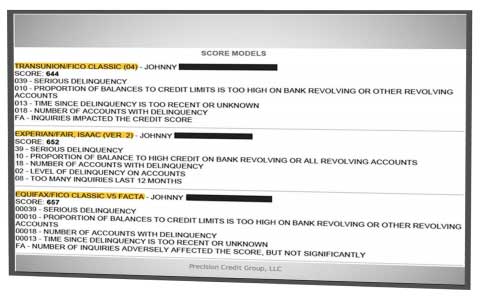

Did you know? There are different credit calculations. There are multiple versions of the FICO score. While it is true that mortgage companies use FICO scores, it is important to understand which FICO scores they are using. Mortgage companies use FICO Classic 04, Fair Isaac V2, and FICO V5 FACTA. Banks, credit card companies, and car finance outlets often utilize a FICO score —- the FICO score they offer is much different from the mortgage score. For instance, they typically use FICO 8 or FICO 9. There are literally hundreds of different credit score algorithms or calculations. Credit Karma is a Vantage Score.

Car finance companies typically use what is called an “Industry Option FICO” which was designed by FICO specifically for car financing. The most common differences in these scores is the way they calculate and factor in medical debts and credit card utilization ratios.

Why is the Credit Karma score that you get a hundred and fifty points higher than what was given by your mortgage broker?

The reason is simple.

There are literally hundreds of different credit score algorithms or calculations in use today.

Typically the consumer credit score, the one you get from places like Credit Karma or freecreditreport.com are going to be significantly higher than what a mortgage broker pulls because those algorithms are stricter.

So even with the exact same information on your credit report depending on where it’s pulled you’re going to get a very different score.

Why is it that when the mortgage broker just pulled your credit or when you viewed it yourself at the car dealership you have three different scores?

Why is there often a big of a discrepancy between the three credit bureaus?

The answer is simple – not all things report to all three credit bureaus…

For instance if you have a collection account that’s with a small local collection agency they may only choose to report to one of the three bureaus.

For example, maybe they only report to Equifax and that’s why the score is so much lower with Equifax.

{kind=link}